An organisation can be required to undertake either a financial audit, financial review, or agreed-upon procedure engagement (AUPE) for a variety of reasons, including statutory requirements or to meet the stipulations made in trust deeds, constitutions or charters. When given the choice between an audit, review or AUPE, it’s important to understand the difference and therefore which is right for your entity.

An organisation can be required to undertake either a financial audit, financial review, or agreed-upon procedure engagement (AUPE) for a variety of reasons, including statutory requirements or to meet the stipulations made in trust deeds, constitutions or charters. When given the choice between an audit, review or AUPE, it’s important to understand the difference and therefore which is right for your entity.

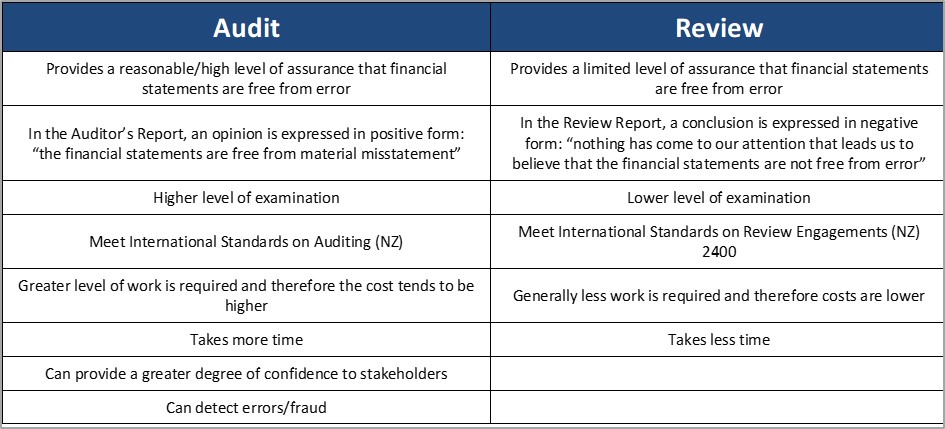

What Is An Audit?

An audit is an objective, independent examination of the financial statements, records, operations, inventory (and so on) of an organisation. The purpose is to provide assurance that the financial statements are free from error and that the entity conforms to the applicable financial reporting framework. The audit primarily determines whether the financial statements represent a true and fair view, and secondly aims to detect any errors or fraud. An audit provides a reasonable or high level of assurance.

What Is A Review?

A review is an evaluation of an organisation’s financial data for the purpose of providing assurance that the financial statements are free from material misstatement. It requires a lower level of examination than an audit and therefore is less detailed, with the auditor not required to have in-depth knowledge of the organisation’s internal control systems. Because of these reasons, a review provides limited assurance.

The Differences Between Audits And Reviews

Agreed-Upon Procedures Engagement

If your organisation does not require an audit or review but does need a professional, qualified Chartered Accountant to verify factual information then an AUPE may be suitable.

An AUPE is a professional engagement in which a Chartered Accountant agrees with the client to perform specific procedures with respect to information. In such an engagement, the Accountant reports the factual findings resulting from the procedures performed.

The level of assurance given by the Accountant in an AUPE will depend upon the nature of both the specific engagement and the specific procedures requested by the client, and the nature and extent of the verification work performed by the Accountant.

If your organisation has the option of undertaking an audit, review or agreed-upon procedure engagement, the UHY Haines Norton Audit team can work with you to decide which is right for your organisation. We can help you to weigh up the level of assurance your organisation requires, as well as the cost and time factors, to decide which will be the best option.

Audit Director Bhavin Sanghavi and the UHY Haines Norton Audit team provides audits, reviews and agreed-upon procedure engagements for organisations of all sizes and industries. To find out more about how we can help you, please contact Bhavin on (09) 839-0248 or email bhavins@uhyhn.co.nz.

Audit Director Bhavin Sanghavi and the UHY Haines Norton Audit team provides audits, reviews and agreed-upon procedure engagements for organisations of all sizes and industries. To find out more about how we can help you, please contact Bhavin on (09) 839-0248 or email bhavins@uhyhn.co.nz.